Once you’ve found product/market fit, scaling a SaaS business is all about honing your go-to-market efficiency. Many extremely helpful metrics and analytics have been developed to provide instrumentation for this journey. LTV (lifetime value of a customer), CAC (customer acquisition cost), Magic Number, and SaaS Quick Ratio, are all very valuable tools. The challenge in using derived metrics such as these, however, is that there are often many assumptions, simplifications, and sampling choices that need to go into these calculations, thus leaving the door open to skewed results.

For example, when your company has only been selling for a year or two, it is extremely hard to know your true Lifetime Value of a Customer. For starters, how do you know the right length of a “lifetime”? Taking 1 divided by your annual dollar churn rate is quite imperfect, especially if all or most of your customers have not yet reached their first renewal decision. How much account expansion is reasonable to assume if you only have limited evidence? LTV is most helpful if based on gross margin, not revenue, but gross margins are often skewed initially. When there are only a few customers to service, COGS can appear artificially low because the true costs to serve have not yet been tracked as distinct cost centers as most of your team members wear multiple hats and pitch in ad hoc. Likewise, metrics derived from Sales and Marketing costs, such as CAC and Magic Number, can also require many subjective assumptions. When it’s just founders selling, how much of their time and overhead do you put into sales costs? Did you include all sales related travel, event marketing, and PR costs? I can’t tell you the number of times entrepreneurs have touted having a near zero CAC when they are just starting out and have only handfuls of customers–which were mostly sold by the founder or are “friendly” relationships. Even if you think you have nearly zero CAC today, you should expect dramatically rising sales costs once professional sellers, marketers, managers, and programs are put in place as you scale.

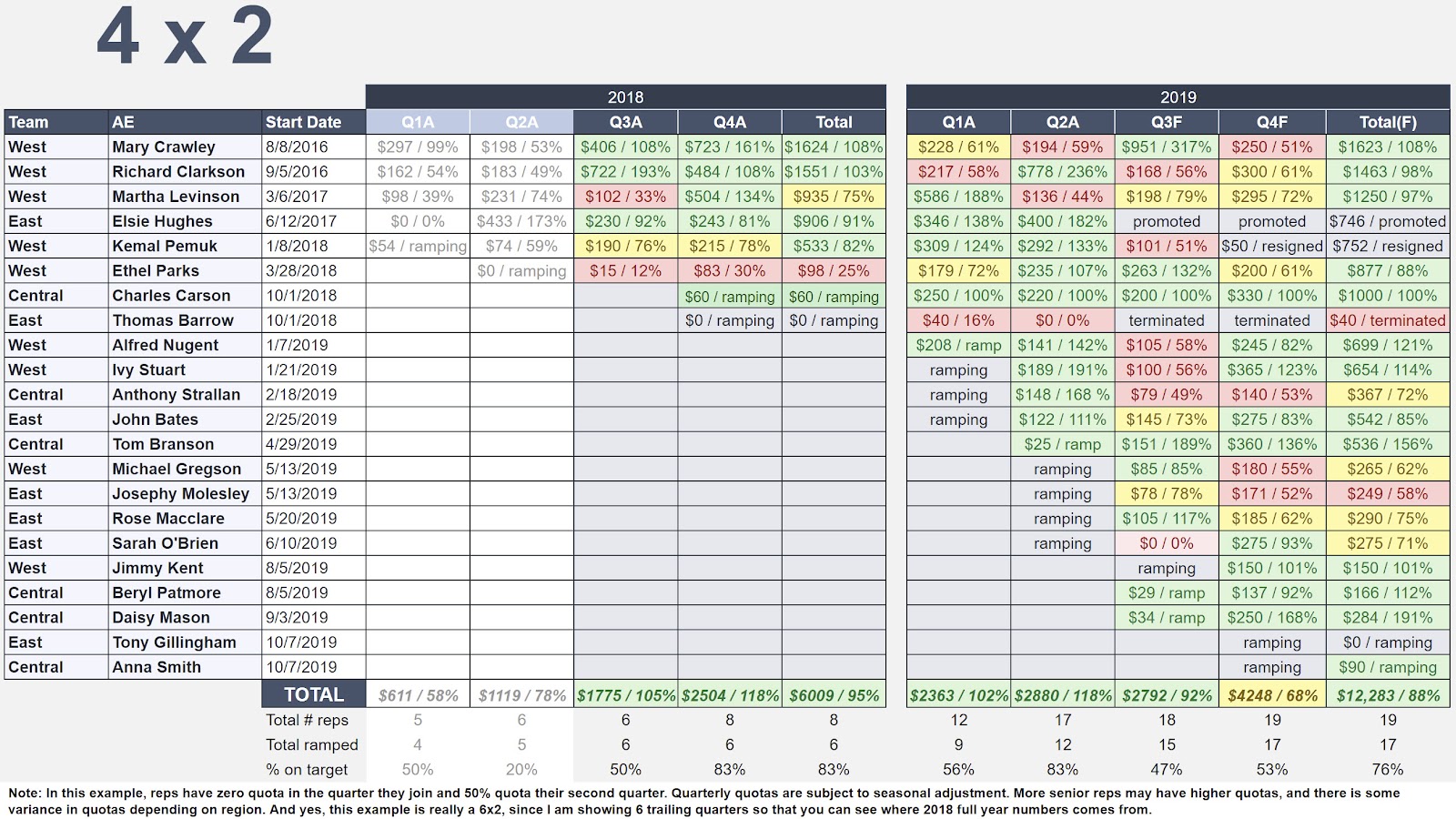

One alternative to using derived metrics is to examine raw data, less prone to assumptions and subjectivity. The problem is how to do this efficiently and without losing the forest for the trees. The best tool I have encountered for measuring sales efficiency is called the 4×2 (that’s “four by two”) which I credit to Steve Walske, one of the master strategists of software sales, and the former CEO of PTC, a company renowned for their sales effectiveness and sales culture. [Here’s a podcast I did with Steve on How to Build a Sales Team.]

The 4×2 is a color coded chart where each row is an individual seller on your team and the columns are their quarterly performance shown as dollars sold. [See a 4×2 chart example below]. Sales are usually measured as net new ARR, which includes new accounts and existing account expansions net of contraction, but you can also use new TCV (total contract value), depending on which number your team most focuses. In addition to sales dollars, the percentage of quarterly quota attainment is shown. The name 4×2 comes from the time frame shown: trailing four quarters, the current quarter, and next quarter. Color coding the cells turns this tool from a dense table of numbers into a powerful data visualization. Thresholds for the heatmap can be determined according to your own needs and culture. For example, green can be 80% of quota attainment or above, yellow can be 60% to 79% of quota, and red can be anything below 60%. Examining individual seller performance in every board meeting or deck is a terrific way to quickly answer many important questions, especially early on as you try to figure out your true position on the Sales Learning Curve. Publishing such “leaderboards” for your Board to see also tends to motivate your sales people, who are usually highly competitive and appreciate public recognition for a job well done, and likewise loathe to fall short of their targets in a public setting.

Some questions the 4×2 can answer:

Overall Performance and Quota Targets: How are you doing against your sales plan? Lots of red is obviously bad, while lots of green is good. But all green may mean that quotas are being set too low. Raising quotas even by a small increment for each seller quickly compounds to yield big difference as you scale, so having evidence to help you adjust your targets can be powerful. A reasonable assumption would be annual quota for a given rep set at 4 to 5 times their on-target earnings potential.

Trendlines and Seasonality: What has been the performance trendline? Are results generally improving? Was the quarter that you badly missed an isolated instance or an ominous trend? Is there seasonality in your business that you have not properly accounted for in planning? Are a few elephant sized deals creating a roller-coaster of hitting then missing your quarterly targets?

Hiring and Promoting Sales Reps: What is the true ramp time for a new rep? You’ll see in the sample 4×2 chart that it is advised to show start dates for each rep and indicate any initial quarter(s) where they are not expected to produce at full capacity. But should their first productive quarter be their second quarter or third? Should their goal for the first productive quarter(s) be 25% of fully ramped quota or 50%? Which reps are the best role models for the others? What productivity will you need to backfill if you promote your star seller into a managerial role?

Evaluating Sales Reps: Are you hitting your numbers because a few reps are crushing it but most are missing their numbers significantly? Early on, one rep coming in at 400% can cover a lot of sins for the rest of the team. Has one of your productive sellers fallen off the wagon or does it look like they just had a bad quarter and expect to recover soon? Is that rep you hired 9 months ago not working out or just coming up to speed?

Teams and Geographies: It is generally useful to add a column indicating the region for each rep’s territory and/or their manager. Are certain regions more consistent than others? Are there managers that are better at onboarding their new sellers than others?

Capacity Planning: Having a tool that shows you actual rep productivity and ramp times gives you the evidence-based information you need to do proper capacity planning. For example, if you hope to double sales next year from $5M ARR to $10MM, how many reps do you need to add–and when–based on time to hire, time to ramp, and the percentage of reps likely to hit their targets? Too few companies do detailed bottoms up planning at this level of granularity, and as a result fail to hit their sales plans because they simply have too few productive reps in place early enough.

There are many other questions the 4×2 can shed light on. I find it especially helpful during product/market fit phase and initial scaling. We tend to spend a few minutes every board meeting on this chart, with the VP Sales providing voice over, but not reciting every line item. As your team gets larger and the 4×2 no longer fits on one slide, it might be time to place the 4×2 in the appendix of your Board deck for reference.

One question often asked about implementing the 4×2 is what numbers to use for the current and next quarter forecasts? If your sales cycles are long, such as 6 months, then weighted pipeline or “commits” are good proxies for your forward forecasts. In GTM models with very short cycles, it will require more subjective judgement to forecast a quarter forward, so I recommend adding a symbol such as ↑, ↔, or ↓ indicating whether the current and forward quarter forecast is higher, lower, or the same as the last time you updated the 4×2. Over time you’ll begin to see whether your initial forecasts tend to bias too aggressively or too conservatively, which is a useful thing to discover and incorporate into future planning.

There are lots of ways to tweak this tool to make it more useful to you and your team. But what I like most about it is that unlike many derived SaaS metrics, the 4×2 is based on very simple numbers and thus “the figures don’t lie.”

To Measure Sales Efficiency, SaaS Startups Should Use the 4×2 was originally published on TechCrunch‘s Extra Crunch.

{kind=link}